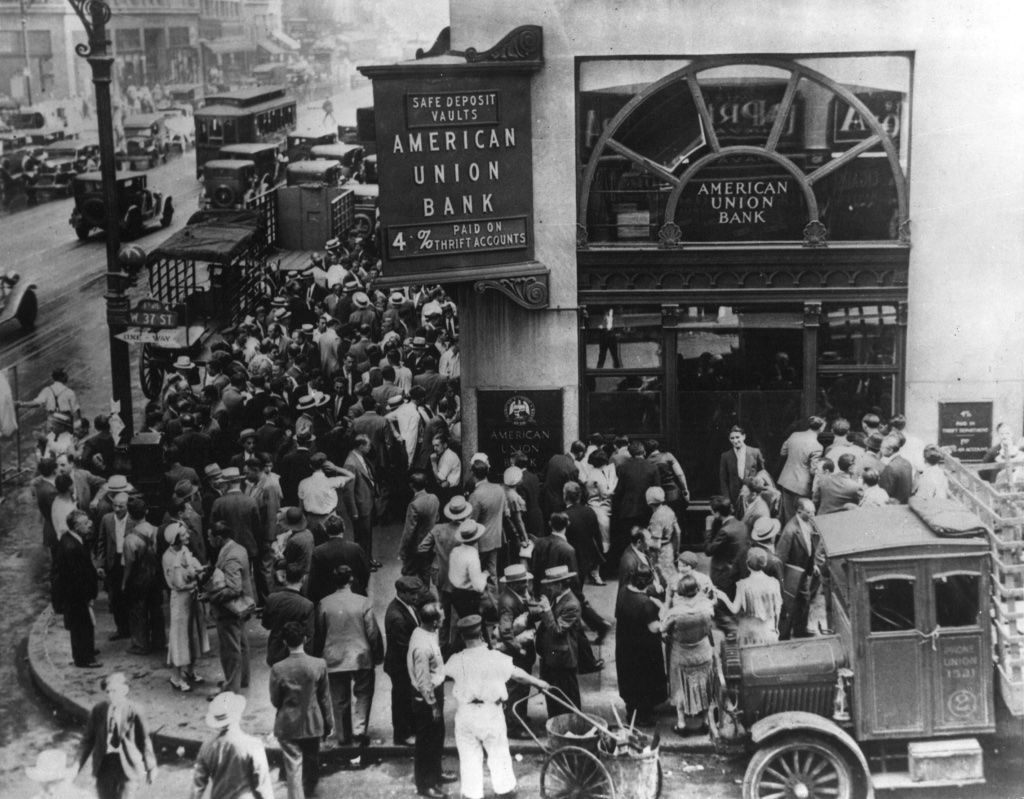

For those of us in tech or in finance, the story of the week has been the bank run on Silicon Valley Bank. Thousands of the Silicon Valley running on fumes VC funded startups were at risk of not meeting payroll. In the rest of the world, startups are expected to become profitable in fairly short order or keep their expenses down. But not in California.

Silicon Valley profligacy, embodied in the VC drive to traction instead of sustainability and profit and IPO-centric management, mean a company like Telegram runs with 60 core staff, while Twitter’s head count before Elon Musk was over 6000. Post-Elon, Twitter is now down to about 1000 employees. Twitter has about 550 million active users. Telegram has over 700 million active users. AirBnb

VK’s headcount ballooned from approximately 3000 to 10000 between 2015 and 2021. There’s quite a few cushy jobs for sons and daughters of the elite and politicians in that kind of headcount expansion. It’s still a tiny fraction of the Facebook/Meta headcount, where 10000 jobs is a single layoff cycle. There’s still 86000-odd Meta employees.

In the short term, the small army of venture capitalists and access to easy finance like Silicon Valley Bank and Soft Bank make the US tech sector stronger. In the long term, it means the US is building inefficient company after company none of which can pay its bills as it goes. When the VC’s advising a given unicorn decide it has accrued a sufficient traction (userbase to monetise), the boom drops like a guillotine on the neck of its poor users.1

What has the US government decided to do in the face of a bank run on Silicon Valley Bank? The cheerleaders for capitalism at the FDIC (Federal Deposit Insurance Corporation) and the Federal Reserve took the decision to backstop all bank deposits:

What is more notable is that the BTFP – or Buy The F…ing Pivot – facility, will pledge collateral at par, not at market value, thus giving banks credit for all those hundreds of billions in unrealized net losses, and allowing banks to “unlock liquidity” based on losses which the Fed and TSY now backstop!

Effectively, assets go onto the balance sheet at whatever price the bank chooses to give them.

On the plus side, neither bank shareholders nor bank officers will be protected:

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Unfortunately, removing protection for shareholders and the bank executives themselves runs a strong risk of turning a bank license or executive position into a visit to the casino with unlimited chips. This is what haappened in the Russian banking system in the Wild East of the 90’s.

Enterprising ex-Komsomol finance students would finagle a banking license. They would offer fabulous rate of return for hard currency deposits – say 8% or 10%. Over three or four years (fewer if the bank directors were less patient), the bank RosCapitalBank (imaginary name but they all had names like this) would accrue a sufficient amount of assets to allow them to build a large loan portfolio. Then the bank would make soft loans to friends and partners on massive projects with weak collateral terms.

At the first sign of crisis, the bank would have to produce more capital. Since their loan portfolio was soft, the bank could not do so. The bank would go bankrupt, the depositors would not get their money and the loans would mostly remain uncollected. Or by the time, they were collected in converted rubles, the loan was more or less worthless. Effectively the loan had been liquidated by inflation.2

The core similarity is that the bankers got rich not by prudent management and a long term vision but via graft and favour. Bankers should be colour-blind and no one’s friend, not a silent partner in every business they fund. The bank’s participation should be via the loan and not via reverse-backscratching and pots-au-vin.

This change in US banking to reward lax banking and patronage will inevitably lead to both more corruption and more carelessness. Reward failure and/or corruption and you will get more failure and corruption. The money to pay for all of these guarantees and backstops must come from somewhere. The US Treasury says none of the money will come from taxpayers or the federal budget:

Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.…We are also announcing a similar systemic risk exception for Signature Bank…All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

In literal terms, there is some truth in this claim. Most of the money to pay for these policies will not come from an already overstretched tax system. Where the money will come from will be from the printing presses. The Federal Reserve will print whatever money it must to be able to return funds to depositors. Printing money leads to inflation, which post-Covid we are already seeing both in the US and Europe. During the Covid period, governments recklessly relied on the printing press to fund both missing tax revenue and new spending commitments. Inflation at over ten per cent has been the result. This level of inflation has not been seen since the late 1970’s and the early 1980’s.

Printing money to pay back depositors takes the US economy another step further to printing press financing and hyperinflation. The cure (guaranteeing all deposits at all banks) will be worse than the disease (short-term financial crisis in Silicon Valley). The disease left to run its course would have encouraged bankers to seriously consider how they handle both loans and investments to ensure that they are prepared for a bank run.

The venture capitalists hollering for unlimited support for Silicon Valley Bank should have been doing their job and protecting the assets of the companies in which they invested. The VC’s have enough financial resources to protect their fledglings. It’s just that the VCs don’t want to pay for their mistakes. Instead, Main Street will again be stuck with the bill for California’s and New York’s carelessness. One small step forward for banking in this case is a huge step forward on the path to hyperinflation.3

-

Remember YouTube which was a splendid platform with likes and dislikes and very little censorship which only ran the occasional ad? The only way to use YouTube without losing one’s mind these days is to pay Alphabet €10/month for YouTube Premium. Otherwise it’s endless video ad after video ad. ↩

-

When the wrong people had soft loans and the right people acquired the portfolio, people died for not paying back their loans or bankers died for demanding repayment. It was a mess. Bankers lived their lives on the run. One of their essential household budget items was personal security and bodyguards. ↩

-

Why has the USD not foundered in recent years in the face of such loose monetary policy and such a poorly managed balance sheet? Since Europe is running the same kind of loose money policy that the US has adopted, there is nowhere for prudent money to go. Apparently the Swiss have not bought into the printing press economy yet. The price of the Swiss Franc reflected their stubborn prudence until, ironically enough, in November 2022 a banking crisis surfaced at Credit Suisse. ↩